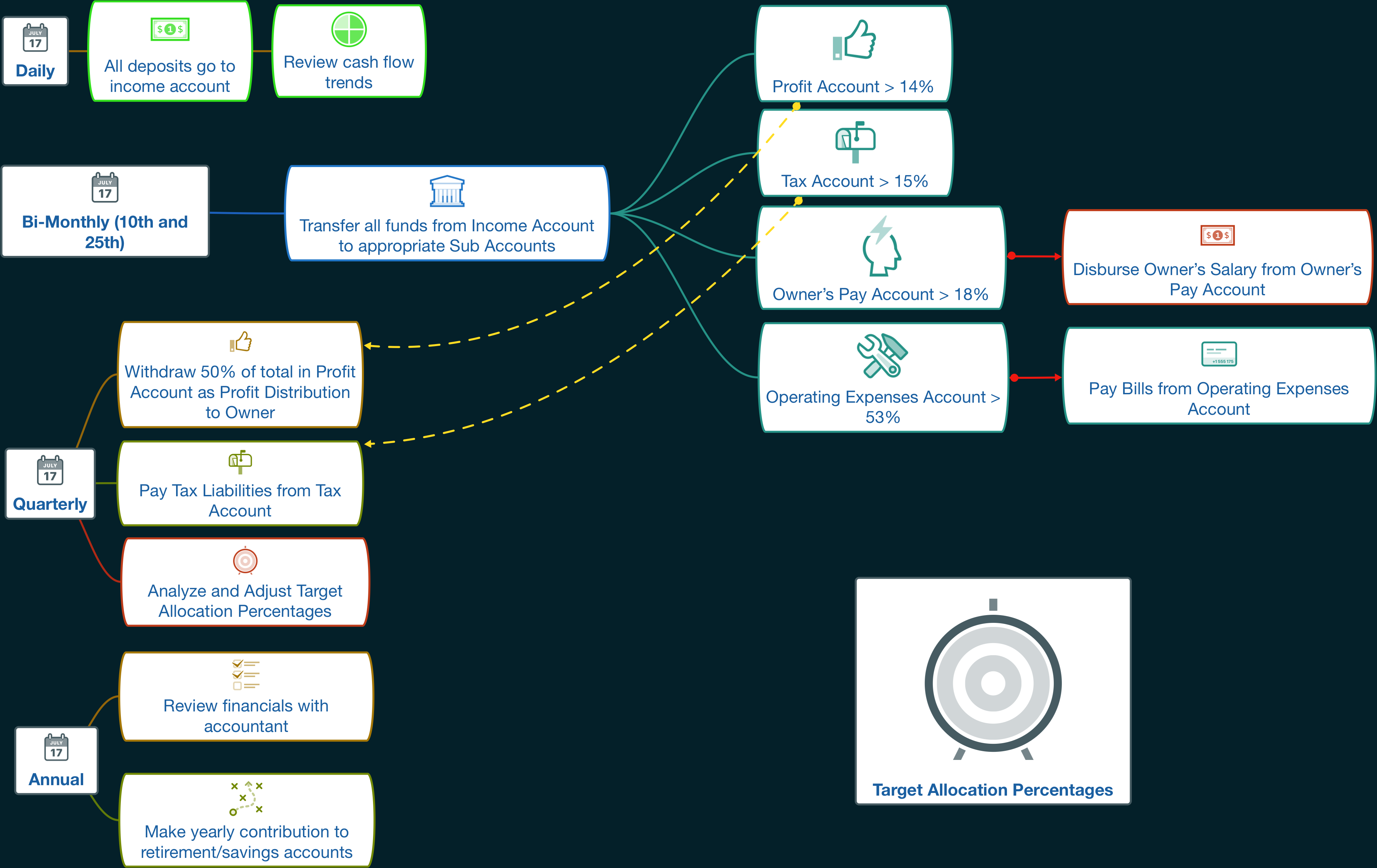

i think i’m going to start with this:

14% profit

15% tax

18% owner’s pay

53% ops

kind of conservative, but it will be nice and easy while i get a feel for it.

i think i’m going to start with this:

14% profit

15% tax

18% owner’s pay

53% ops

kind of conservative, but it will be nice and easy while i get a feel for it.

Thanks. I put the book on my wish list, along with enough revenues to use it.

Nice post Brian. I was reading the titles of the books on the shelf from left to right, and got a nice suprise when I got to the end.

Have you read “Entreleadership” by Dave Ramsay?

He has a lot of good ideas for building a solid business.

I’ll check it out

I’ll check it out

Just got Profit First last week, haven’t started it yet though

2015 Budget / Allocations Totals as % of Gross Revenue :

All Marketing/ Ads 1.5%

All Insurance 1.3%

Vehicle ( Gas / Maint. ) 9%

Accounting / Professional Services 2%

Payroll ( Employee Net Pay ) 20%

Payroll ( All Taxes ) 4 %

All other misc.( see below) 1.5%

Estimated Pre tax net profit 20.7 %

Notes:

There have been some questions of FB about the need for a separate bank for tax and profit accounts. The flow chart i posted before is an exact representation of the Profit First model as recommended by the author. You can, however, tweak it however you want. Below is a version that excludes the second bank and off-site accounts in favor of just one bank with sub-accounts.

this would in theory accomplish the same thing. just remember- the Profit First method is every bit as much about leveraging basic human behavior and habits (something common GAAP accounting methods totally ignore) to make your money do what you want it to, as it is about just moving money around and keeping organized.

there’s a very specific reason that two separate off-site bank accounts are recommended, and it has nothing to do with accounting. here’s a direct quote from the book that sums it up better than I can:

"PARKINSON’S LAW

Author and historian C. Northcote Parkinson theorized that our demand for a resource increases to meet

the supply of it. That is why when we are given two weeks to do a project it takes two weeks, and when

we are given eight weeks to do the same project it takes eight weeks. That is why when given $1,000 to

complete our work we get it done with $1,000 and when given $10,000 to complete the same work, it

takes $10,000. Profit First makes Parkinson’s Law an asset. By taking profit first the money available for

expenses lessens, and we are forced to find ways to get the same things done for less money…

…DON’T CHANGE HABITS, LEVERAGE THEM

Many entrepreneurs try to force themselves to become better at accounting and to become more disciplined

in their fiscal management by pure willpower. But just like a muscle, willpower can be drained. And in a

moment of financial stress or bigger than expected expenses the entrepreneur will break their own fiscal

rules and spend the money they have. The Profit First principle does not try to change your habits (that is

nearly impossible to do), Profit First works with your existing habits. By first allocating money to different

accounts, and then removing the temptation to “borrow” from yourself, your business will become fiscally

strong and you will benefit from regular profit distributions.Target Allocation Percentages v2.0.pdf (151.1 KB)

I thought I’d weigh in with our ‘profit first’ approach, as an owner/operator company. I know this thread is more aimed at those with employees, but truthfully, most window cleaners are ‘still one-man-shows’, so this might be helpful to some guys or gals here:

First, we use virtual sub-accounts for our accounting (we seem to have the self-control for it, but if you don’t, then by all means use real accounts. The virtual accounts allow us to setup ‘mini-funds’ on the fly, though). We have 3 real accounts with the same local bank

Instead of making transfers based on a set percentage each week, we use flat dollar amounts based on our projected yearly income (adjusting as necessary). We make all of our contributions to the savings/taxes/profit accounts during the ‘in-season’ weeks, and none during off-season.

we give ourselves a fixed weekly salary based on our actual living expenses, plus a reasonable amount for discretionary spending

Here’s how our percentages are looking for 2016:

When I get in front of my computer, I might upload our savings/contribution plan for the in-season period, as it also acounts for saving up enough salary for the out of season/vacation weeks.

Profit 8%

Owners Pay 62%

Tax 8%

Operating 22%

This thread has literally transformed my business for the better. Thanks again Caleb.

I’d like to see how you proportion that, for some ideas Alex

It’s a great approach since it really forces a person to be on their game with pricing etc to make it all come together to work

If a one person operation gets set up like this on the right foot, it’s setting the foundation for hiring, growing, selling or even just maximizing one’s own results

Love the mind map… I need to learn how to do these… I still use my many many whiteboard everyday

Well, this is my first year of implementing this from the get-go, so I’m sure I’ll need to make some refinements as the year progresses. But at this point, what I’ve done in my overall budget/income projection spreadsheet is this (I’ll probably be repeating myself a little, but bear with me):

I have a real-world figure of what our personal salary needs to be every week.

I’ve done all the math on what I want our yearly gross to be (a little less than last year)

I’ve divided our projected income into 3 categories:

I have the spreadsheet currently setup so that I can easily change the number of each type of week, but they currently are:

Then I take the yearly figures for (1) profit, (2) taxes, and (3) what we need to save to cover our winter salary, and divide it by 30 (our number of in-season weeks)

But in practice, I know that not every week will be the same. Some weeks we will exceed our income goal, and other weeks we will fall short. So what I’m thinking of doing is pulling our weekly salary first, since it’s a fixed amount, plus a fixed amount for business expenses, and then divvying up the remainder into the virtual savings accounts:

So to recap, setting the money aside in the above manner means that during the winter slowdown, any income we bring in only needs to go towards our personal salary. At that point all the money has already been set aside for our profit, taxes, and operating expenses. If we exceed our income projections for the winter, we’ll be using that income towards our personal salary, and leaving our winter savings alone to cover any increase in taxes.

Hope this helps anyone in similar shoes, that doesn’t like to go hunting for work during the winter

Thanks for sharing Alex. I like this break down.

I think the salary part is doable since it will be a fixed amount, but business expense can and will fluctuate.

This thread is very good, just saying. ![]()

Our personal expenses fluctuate, as well. It all comes down to budgeting. Essentially we’d be giving the business its own little “salary”, as well, just for the day to day, month to month costs. Any major expenses would probably come out of the profit account- similar to how we have virtual accounts setup for our larger personal expenses.

Hope that makes sense ![]()

thanks, love the ideas

what exactly is the out of season week range where you live?